Updated: April 20, 2022

Updated: April 20, 2022

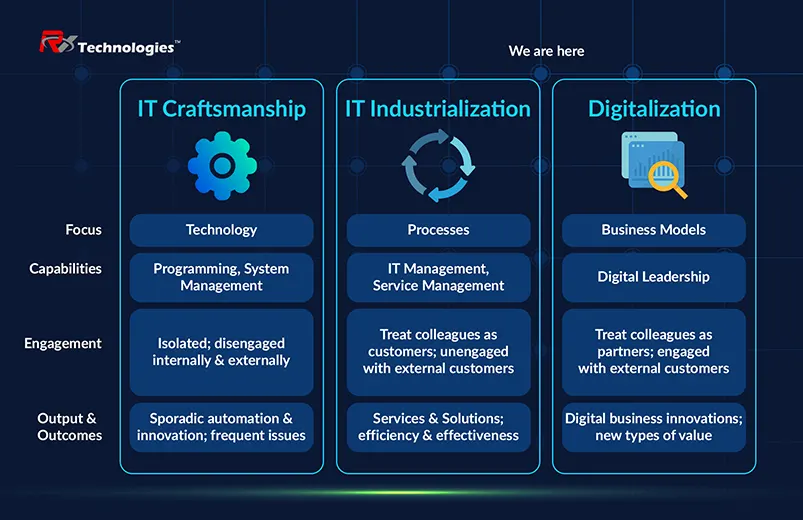

The Three Phases of IT-enabled Business Transformation

The first phase of IT-enabled business transformation during the 1960s and 1970s automated individual activities, leading to increased productivity and efficiency. The automation of activities enabled by software led to new data being captured and analyzed in each activity, leading to the standardization of processes.

The second wave of IT-enabled business transformation in the 1990s was due to the internet’s inexpensive and ubiquitous connectivity, which made access to information easier. The internet applications altered the traditional business value chain, reducing entry barriers and creating new substitutes leading to higher competition in the market.

In the third phase of IT-enabled business transformation, information technology is becoming an integral part of the product, removing the distinctions between different industries.

Three Phases Of Banking And Financial Services Evolution

Banking and financial services have always been information-intensive, and their core products and processes have high information content. They were the earliest adopter of information technology in their business to gain a competitive advantage. The first generation of banking and financial services transformation was implementing core banking solutions primarily developed in-house towards the end of the 1970s that offered a few basic features, such as customer data management, transactions, record-keeping, etc.

In the second generation of banking and financial services transformation, the internet-enabled institutions offer online channels to customers to access banking services. It also led to new competitors, commonly referred to as Fintech, which were essentially internet-powered platforms that leveraged technology innovation and data power to disrupt specific financial services business areas.

The third generation of banking and financial services transformation is characterized by the embedding of financial services such as payments and lending within core products of non-financial companies to make their core offerings more attractive. These non-finance companies are referred to as TechFin, essentially internet companies from diverse businesses such as e-commerce, telecommunications, search engines, social media platforms, gaming companies, etc.

Fintech and TechFin will continue to disrupt the financial services sector. We look into FIntech vs. TechFin differentiation and assess how the two will shape the future of finance and the economy.

What is Fintech?

Fintech companies’ core business is financial services, even as the term is generally used for technology startups disrupting banking and financial services.

Fintech startup takes a focussed approach by identifying lacunae or inefficiency in the existing processes and using emerging technologies to solve the problem. Fintech leverages API (Application Programming Interface), Artificial Intelligence (AI) and machine learning (ML), Blockchain to create innovative solutions in different areas of financial services such as payments, lending, money transfers, investment advisory, and open banking. FinTech development will guide the business model innovation in the broader banking and financial services industry.

FIntechs can be broadly classified into the following categories

- Accounting & Finance

- Asset Management

- Business Lending & Finance

- Capital Markets

- Core Banking & Infrastructure

- Credit Score & Analytics

- Crypto

- Financial Services & Automation

- General Lending & Marketplaces

- Insurance

- Mobile Wallets & Remittances

- Payments Processing & Networks

- Payroll & Benefits

- Personal Finance

- POS & Consumer Lending

- Real Estate & Mortgage

- Regulatory & Compliance

- Retail Investing & Secondary Markets

Neobanks, another type of Fintech, are internet-only or digital banks that operate exclusively online without any physical branches. They offer personalized services to customers leveraging technology and artificial intelligence while minimizing operational costs. Even as Neobanks have added customers quickly, their impact on the financial services industry is yet to be ascertained.

Even the incumbent financial institutions also leverage emerging technologies to offer their customers differentiated products and better services. Still, they have legacy issues that do not offer them flexibility, as the emerging Fintech. Online and mobile banking are incumbent financial services institutions’ most common Fintech solutions.

What is TechFin?

TechFin includes technology companies whose core business specimen does not finance, but they embed financial services in their core products to make them more attractive. These companies want to leverage their existing customer relationship and behavioral data to disrupt the banking and financial services business. Access to customer data is the most critical advantage of these companies.

In the initial phases, TechFin is interested in the distribution side of the financial services business even as they are content with banks managing the regulatory compliance requirements. They are interested in gaining access to customers’ financial transaction data, which adds diversity to their existing customer data and offers them a real picture of customers’ finances.

Each tech company has different customer data. Social media companies have user social preferences and activities, and e-commerce companies have data on customer demand, purchases, and payment history. Google has data on practically all aspects of customer life, while telecommunication companies such as Apple have data on user behavior, location and activities. TechFin companies are interested in enriching existing customer data with transactional information to improve their core offering further and provide complementary financial services.

The platform-centric data-driven business models of TechFin are independent of the margin generated from financial services. Hence there are greater challenges to banks and financial services companies than Fintech.

Fintech Vs. TechFin: Key Differences

Unlike Fintech, TechFin leverage captive customer data

Fintech companies don’t have a captive customer base and data or brand loyalty when developing solutions. In contrast, TechFin starts with an advantage of a loyal customer base and the vast volume of data already collected.

The Difference in key business objectives

Another area of differentiation is in the context of the primary business objectives of Fintech and Techfin. FinTech’s key business objective is to provide a better customer experience by using digital technologies that reduce friction and cost for customers while offering additional features and benefits. Fintech’s core business is financial services, and they are dependent on margins for profitability.

TechFin’s key business objective is to complement its core product and services by expanding into a complementary financial services business. Unlike Fintech, these firms don’t exclusively offer financial services, and hence they are not dependent on margins for their profitability.

Unlike Fintech, TechFin is in a driver’s position to collaborate with mainstream banks and financial institutions.

TechFin, with a loyal customer base and data, is in the driver’s seat to challenge mainstream banks and financial institutions more than Fintech. This realization is not lost on the incumbent financial services companies collaborating with tech giants, even if it means sharing distribution income and valuable data. TechFin usually starts with payment solutions and later adds complementary products and services to generate incremental revenue.

Google has expanded the scope of financial services by partnering with Citibank to allow its users open checking and saving accounts and intends to extend the collaboration to ten other banks and credit unions in the United States. Google’s co-branded service with Citibank is Citi Plex, which offers checking and savings accounts with no monthly fees, overdraft charges, or minimum balance rules. Similarly, Apple launched its iPhone-integrated credit card with Goldman Sachs. Amazon leverages data to underwrite small loans for merchants, consumers, and SMBs.

Even as the Fintech and Banks partnership has increased in recent years, the partnership is falling short of financial institutions. Only 28% have realized a 5% or better increase in loan volume. The increase in revenue from new products due to partnering has been even with only 14% realizing at least a 5% gain in revenue.

How will Fintech and TechFin impact the future of the financial and economy?

Digitization of financial products and asset classes

All financial products and asset classes will be digitized whether used by retail customers, small and medium enterprises (SMEs), or large institutions. The initial phase of digitization covered standard products and services such as equities and government bonds and consumer banking products such as payments, loans, brokerage services, and auto insurance.

Fintechs will lead the second phase of digitization across consumer banking, SME and commercial, financial services, capital market, mortgage market, and fund management. Mobile applications will be the enabler of digitization initiatives across different business segments.

A successful Fintech app development requires business domain knowledge and technical expertise for mobile app development. It is beneficial for a fintech or financial services institution to outsource app development to an experienced mobile app development company.

Embedded financial services within the software and marketplace solutions

The embedding of financial services enhances the core product and service offerings while significantly increasing the addressable market for platform companies from different industry segments. Embedded financial services will continue to be adopted by several companies beyond the top platform companies.

Some prominent company categories that have embedded financial services are:

- Marketplace ecosystems were the first to embed payments and lending to complement their core services and create new monetization opportunities. The category includes B2C marketplaces and e-commerce enablement platforms, and vertically oriented B2B marketplaces. The companies in this category include Amazon, Shopify, and others.

- Vertical software vendors such as content management systems, point-of-sales, and hospital management systems are embedding payments into broader software products that historically focus on business processes and customer interactions.

Flywire is a feature-rich software suite that serves the education, travel, and healthcare verticals. These have bespoke payment needs that are not adequately served by the horizontal platforms. Flywire enables institutions to receive payments from foreign and domestic students across several multiple payment methods in the education vertical. Similarly, Flywire embeds bespoke financial services within their broader software suite in the healthcare and travel vertical. The embedded financial services enable clients to get a better return on investment(ROI) relative to payment platforms and banks.

- B2B “systems of workflow” that accounts payable/accounts receivable automation, procurement, travel & expenses, treasury management. The embedding of native payments options provides customers with seamless execution and back-end reconciliation accelerating the shift to digital payments within B2B industry segments. The embedded financial services enable software vendors to offer interconnected services to the customers and part of the bank’s profit pools.

As companies consider the ecosystem business model based on its value-generating potential, Fintech app development capabilities will be critical for the strategy’s success. As the companies tried to replicate the ecosystem success of technology giants like Google, and Amazon, they have struggled to realize the value. Companies need to focus on their core competencies by directing their efforts on defining ecosystem strategy and outsourcing app development to specialist mobile app development companies. These companies have the technical expertise and broad capabilities across application development methodologies, performance, and quality tools.

Digital payments innovation and evolution

According to a McKinsey estimate, global payments will total $2.5 trillion in 2025. The enormous opportunity in payments makes it an ideal business segment to target for innovation and disruption by both Fintech and TechFin. We profile the rise of three online payment innovators that have set the agenda for broad-based digital disruption in the banking and financial services industry.

PayPal

The first fintech company with a significant impact on the payments business and heralded the digital disruption of the banking and financial services industry. The customer-centric company simplified the online payment for e-commerce sites like eBay, which depended on checks and cumbersome credit card payments.

After establishing itself as a leading e-commerce payment solution company, PayPal launched business accounts in 2000, allowing businesses to accept unlimited credit card payments. It pioneered cross-border payments and money remittances and remained one of the key online payment companies.

Square

After a decade of PayPal, the company pioneered the technology innovation in point-of-sale systems to allow small and medium businesses (SMEs) with low transaction volumes to accept card payment with its mobile phone-enabled card reader.

After amassing merchant data, Square went to expand into SME lending (Square Capital), rewards (Square loyalty), payroll services(Square Payroll), and other allied services.

Stripe

The company started with a core offering of e-commerce payments processing in 2010 when payments were a nascent market. In the last decade since its founding, Stripe has expanded its platform beyond payments processing to broad-based product and services offerings across the entire payments stack. Stripe has leveraged innovation, strategic business partnerships, acquisitions, and investment in new companies.

Stripe has partnered with Barclays, Citibank, and Goldman Sachs to offer business banking-as-a-service. It has partnered with Afterpay to include buy-now and pay-later checkout for its online payment services. Stripe also offers complementary services such as Stripe Atlas that help entrepreneurs create US incorporated businesses quickly, cutting through inefficient processes.

As a result of its innovative product services, Stripe has seen exponential growth, and it works with companies globally across industry verticals, company sizes, and business models.

The pandemic has accelerated digitization, and we will continue to see Fintech and TechFin redefine the broader banking and services industry with their technology innovation. The next decade will witness a new financial service landscape, with digital becoming the most dominant channel for businesses and individuals.